A quiet drive on a sunny afternoon in the Sunshine State can change in a heartbeat. The sound of screeching tires stays with you long after the dust settles. Once the sirens fade and you return home, a new challenge begins. You receive a call from a person who sounds professional and perhaps even kind. This person is the insurance adjuster.

We want you to understand the way professional agents analyze damage reports and medical costs after a wreck. Carter Injury Law sees how these interactions shape lives every day.The process of valuation is about what the insurance company can justify paying while keeping their profits high. They look at your medical records and the police report. Every piece of data fits into a larger puzzle. Knowledge is your best tool in this situation.

1) Core Logic Behind Claim Valuations

The foundation of any case starts with the insurance policy. An adjuster reviews the limits of the coverage first to know the maximum amount the company might have to pay. However, their goal is to keep the payout far below that limit. They look at the facts of the accident through a lens of risk. They ask if a jury would find their driver responsible and look for any reason to blame you for the impact.

We see adjusters start with a skeptical mindset. They treat every claim as a potential drain on company resources. This is simply their business model. They use standardized methods to ensure that every office follows the same rules. This makes the process feel cold and mechanical. However, we know how to work within that system to highlight the human side of your story.

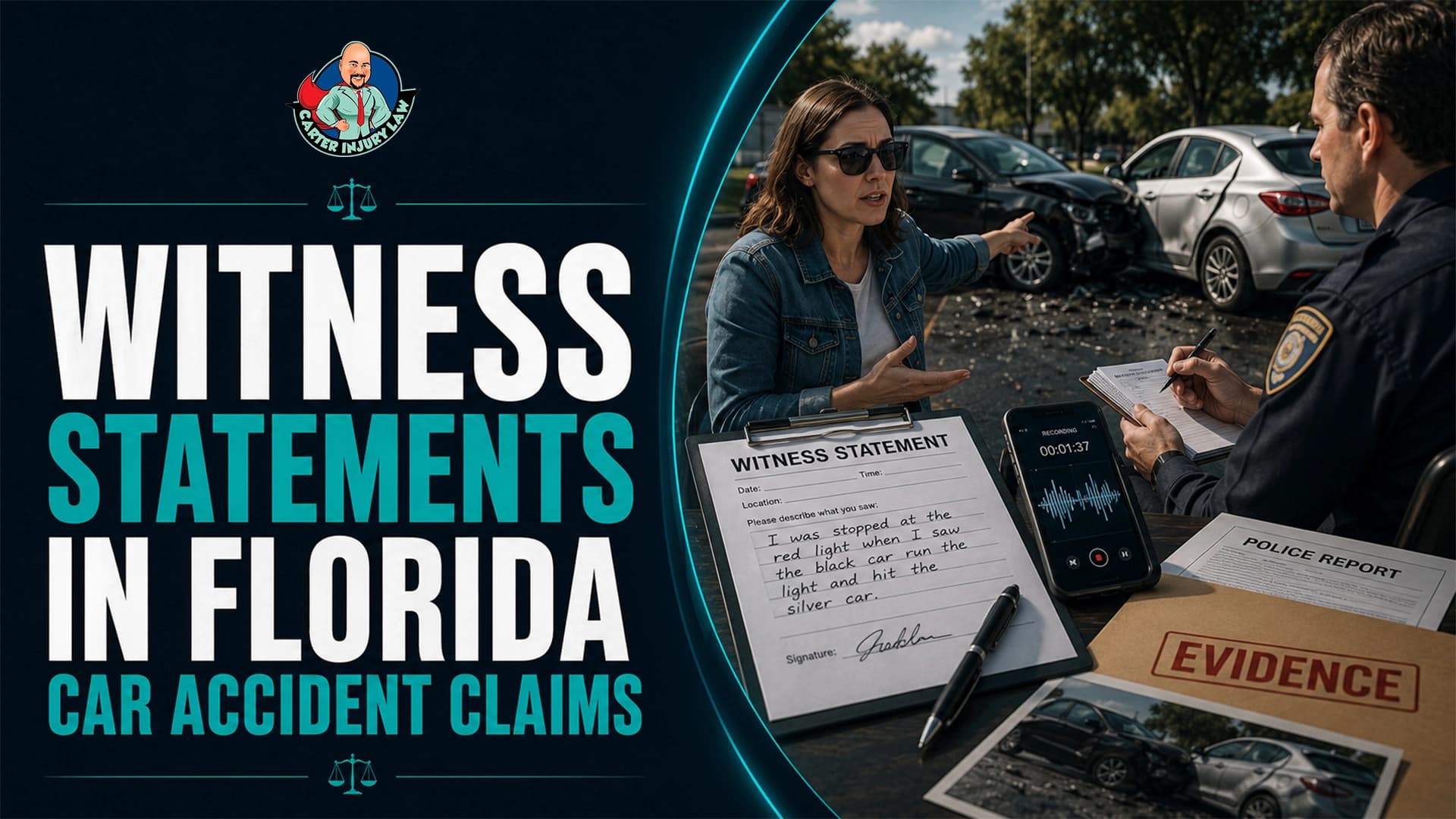

2) Immediate Steps for a Valid Claim

The initial stages of a claim are often the most critical. Florida has unique laws that dictate how much money is available. The representative begins by looking at the basic requirements of your policy. They check if you followed all the rules from the very start.

The Critical Fourteen Day Window

The first thing an evaluator checks is the timeline of your medical treatment. They look for any reason to deny the claim before it even starts. Florida law is very strict about when you must seek help.

Florida saw 362,063 motor vehicle accidents in 2025 with 235,964 of those resulting in reported injuries.

Source: Florida Highway Safety and Motor Vehicles (FLHSMV)

If you wait too long to see a doctor, the company will claim your injuries did not happen in the crash. They specifically look for the PIP 14-day rule Florida compliance. This rule requires you to seek medical attention within two weeks of the accident to access your Personal Injury Protection benefits. If you miss this window, you lose a significant portion of your initial coverage.

Legal Standards for Severe Injuries

Florida is a no-fault state. This means your own insurance usually pays for your initial medical bills. However, if your injuries are severe, you can step outside of this system to sue the at-fault driver.

The adjuster evaluates whether your case meets the Florida serious injury threshold. This legal standard requires proof of permanent injury or significant scarring. If the company decides your injury is minor, they will offer a very small amount of money. They hope you will accept it and walk away without a fight.

Even small choices, like what you say to an insurer, can influence the outcome of a case. You can read more in this overview of five costly mistakes drivers make after a Largo car accident.

3) How Insurance Software Calculates Florida Car Accident Settlements

How Insurance Software Calculates Florida Car Accident Settlements")

Many people believe a human being sits down and thinks about how much an injury is worth. In reality, modern insurance companies rely heavily on technology. Computer Programs and Data Points

Most large insurance companies use a specific type of program to handle their heavy lifting. The most famous one is known as Colossus insurance software. This program uses thousands of data points to create a settlement range.

The software assigns a value to every injury code in your medical file. However, a computer cannot understand how a neck injury prevents you from sleeping. We know that these programs often ignore the human element of suffering. The company uses the software output as their ceiling for negotiations. They rarely tell you that a machine made the decision for them.

Evidence for Better Results

Because software drives the process, the quality of your medical records is vital. If your doctor uses vague language, the software assigns a lower value. Adjusters look for specific value drivers in your files, such as specialist visits or MRI scans.

We advise our clients to be very thorough when describing their pain to doctors. This ensures the Florida car accident settlement process reflects the actual severity of the situation. Every word in those records becomes data for the insurance company algorithm.

4) How Insurance Adjusters Calculate Economic and Non-Economic Damages

Once the adjuster moves past the software, they look at the hard numbers. They divide your claim into two main categories: economic damages and non-economic damages. They use math to justify their final offer to their supervisors.

Medical Bill Totals and Net Payments

Economic damages are the easiest to calculate because they have a receipt. This includes your hospital bills and lost wages. However, recent changes in the law have made this more complex.

The Florida Transparency in Damages law changed how adjusters look at medical costs. They no longer care what the hospital billed you; they only look at what was actually paid by you or your health insurance.

Accident victims who hire an attorney receive settlements that are nearly 3.5 times higher on average than those who represent themselves.

Source: Insurance Research Council (IRC)

The Multiplier for Mental Distress

The hardest part of the evaluation is the non-economic damage. Companies often use the Multiplier method to find this number. They take your total medical bills and multiply them by a number between one and five. If your injury is life-changing, they use a higher number. If they think you will recover quickly, they use a lower one.

5) Recent Florida Laws That Impact Car Accident Injury Claims

Recent Florida Laws That Impact Car Accident Injury Claims")

The legal landscape in Florida changed significantly in 2023. These changes give insurance companies more power than they had in the past. It is more important than ever to understand the current Florida personal injury claim evaluation factors.

The Fifty One Percent Fault Rule

Florida recently adopted a new standard for fault: the Florida comparative negligence 51% rule. Under this law, if a company can prove you were 51% at fault for the crash, you get nothing. The insurance company will search for any reason to blame you.

Certain roads develop accident patterns due to traffic volume and road design. You can learn more about this issue in “A Closer Look at the Frequent Accidents Along Ulmerton Road.”

Shorter Deadlines for Lawsuits

The state reduced the time you have to file a lawsuit from four years down to two years. Adjusters know this well. They may use insurance adjuster tactics Florida car accident strategies to delay your claim. They might act like they are working on a settlement until the deadline passes. Once the two-year mark hits, your right to sue vanishes.

6)The Final Stages of Your Case

An insurance representative will not finalize a claim until they know the full extent of your injuries. They are waiting for a specific medical milestone to be sure that the case will not get more expensive later.

Maximum Recovery Milestones

The company wants to see that you have reached Maximum Medical Improvement (MMI). This is the point where a doctor says you are as healthy as you are going to get. If you still have pain at this stage, it is considered a permanent injury. Adjusters wait for this report because it tells them there are no more surprise medical bills coming.

Medical Lien Coordination

Many people cannot afford treatment while they wait for a settlement. This is where a Letter of Protection (LOP) becomes important. This document allows you to get medical care now and pay the doctor later from your settlement money. Adjusters review these letters carefully to ensure treatment is necessary.

7) Why Insurance Companies Start With Low Settlement Offers

Why Insurance Companies Start With Low Settlement Offers")

When the evaluation is complete, the representative makes an offer. This offer is rarely their best number. It is a starting point for a long negotiation. They expect you to counter.

They hope a quick check will tempt you to sign away your rights. However, the average car accident settlement Florida victims receive is often much higher when they refuse that first low offer.

In a negligence action, any party found to be greater than 50 % at fault for his or her own harm may not recover any damages.

Source: The Florida Senate (Florida Statute 768.81)

Schedule a Free Consultation With Carter Injury Law After a Florida Car Accident

The days following a car crash are filled with big decisions. You are dealing with pain, car repairs, and the stress of missing work. You do not have to carry the burden of the insurance claim by yourself. Learning how professional agents analyze damage reports and medical costs is the best way to protect your future.

We want to ensure that the insurance company treats your claim with the attention it deserves. If you have questions about your specific situation, reach out for a professional opinion at Carter Injury Law.

Carter Injury Law Contact Details

Address: 1234 Legal Way, Suite 100, Tampa, FL 33602

Phone: (813) 555-0199

Website: www.carterinjurylaw.com

Email: info@carterinjurylaw.com

Disclaimer: This article is for general informational purposes and does not form an attorney-client relationship. For help with any personal injury or criminal case, reach out to Carter Injury Law.