Call US

24/7

Free Confidential case Evaluation

(813)922-0228Call US

24/7

Free Confidential case Evaluation

(813)922-0228Loading...

blog

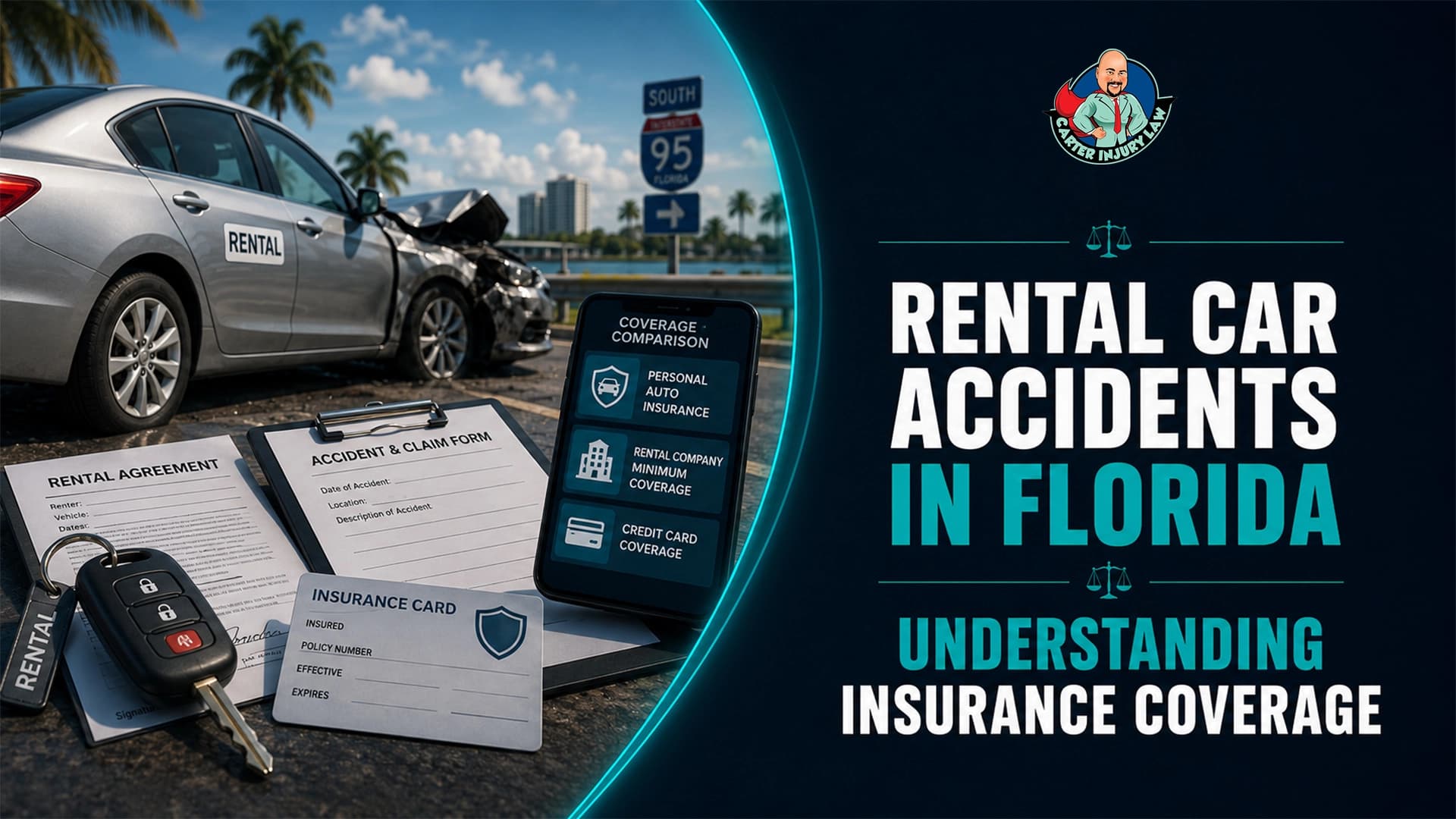

Seeing a license plate from a different state after a collision can immediately spark a sense of panic. You might worry that the legal process will be impossible or that the driver will simply return home and leave you with the bills. Out of State Drivers in Florida Accidents create a unique set of challenges that differ significantly from a typical local crash.

Florida is one of the most visited states in the country, which means local roads are constantly shared by residents and tourists alike. Whether you are dealing with Tampa tourist accidents or snowbird car crashes, understanding how the law protects you is the first step toward recovery.

Florida operates under a strict no-fault insurance system. However, visitors are not required to carry Florida-specific PIP. This creates a coverage gap that often confuses victims during the initial stages of a claim. According to the Florida Highway Safety and Motor Vehicles 2023 reports, thousands of crashes involve out-of-state vehicles annually, making this a common hurdle for local residents.

PIP Limitations. Your insurance typically covers 80 percent of medical bills up to $10,000.

The Tort Threshold. If your injuries are permanent or exceed your policy limits, you may pursue the visitor for additional damages.

Uninsured Motorist Coverage. This secondary protection is vital if the visitor has minimal or no Bodily Injury Liability coverage.

The insurance landscape is complicated by the fact that many visitors come from "Tort" states where PIP does not exist. This creates a conflict of laws that requires a deep understanding of Personal Jurisdiction to resolve fairly.

One of the most powerful tools for a Florida victim is the Florida Long Arm Statute. Specifically, Section 48.193 of the Florida Statutes allows our state courts to exercise authority over people who do not reside here. The law provides that by operating a motor vehicle within the state of Florida, a driver is essentially consenting to the jurisdiction of Florida courts for any accidents they cause.

When a tourist drives on a Florida highway, they enter a legal contract with the state. This contract ensures that they cannot cause harm and then hide behind state lines to avoid a lawsuit. This makes Service of Process on Non-residents a manageable task rather than an impossible one.

You do not have to travel to New York or Georgia to file a lawsuit against the person who hit you. You can handle the entire legal process right here in your home county. This statute ensures that visitors cannot escape their legal responsibilities simply by crossing the state line on their way home.

Procedural Steps for Serving a Nonresident Defendant")

A common fear is that a visitor will simply disappear once they leave the state. To prevent this, Florida law provides a specific pathway for the Service of Process on nonresidents. If a driver has left Florida and cannot be easily located, the law allows you to serve the legal papers to the Florida Secretary of State.

The Secretary of State acts as a substitute agent for the out-of-state driver.

Once the papers are served to the state and notice is sent to the driver's last known address, the legal requirement for service is officially met.

This process ensures the case moves forward even if the defendant is actively trying to avoid being found.

This procedural step is vital for keeping your case on track. It is also important to know how an experienced Tampa car accident lawyer evaluates cases to see if your specific situation meets the criteria for this type of service.

Most states use a system where the at-fault driver is responsible for all damages. Because of this, many visitors carry Bodily Injury Liability or BIL insurance, which is not a requirement for many Florida motorists. This can actually be a benefit for you, as there may be more insurance money available to cover your injuries than if you were hit by a local driver with minimal coverage.

Audit Clauses. Many out-of-state insurance policy limits automatically adjust to meet Florida's minimum requirements if an accident occurs here.

Deemer Clauses. These clauses "deem" the policy to have the coverage required by the state where the crash happened.

Liability Differences. A visitor might have a $50,000 policy in their home state that must pay out according to Florida's negligence standards.

Because the truth about insurance companies is that they will try to find any excuse to deny an interstate claim, identifying the correct policy language is the most important part of the investigation.

The Impact of the Graves Amendment on Rental Car Liability")

Many visitors to the Tampa Bay area arrive via the airport and head straight to a rental counter. Rental car liability in Florida cases is governed by a federal law called the Graves Amendment. This law generally protects rental car companies like Hertz or Enterprise from being held liable for the negligence.

You can't sue the rental company for the driver's mistake unless the company was careless, like renting a car that they knew had mechanical problems. Instead, you need to go after the driver's personal insurance or the rental car insurance secondary coverage they bought at the counter. Visit Florida reports that our state welcomes over 135 million visitors annually, many of whom utilize rentals, making this a frequent complication in local injury claims.

Collecting evidence at the scene is always important, but it is even more critical when the other driver lives out of state. Once they leave the scene, it becomes much harder to get additional information for your file.

Rental Agreement Records. If they are in a rental, take a photo of the contract or the barcode on the windshield.

Permanent Home Address. Do not just get their name. Get their permanent home address and their driver's license number from their home state.

Insurance Card Photos. Get a photo of their physical insurance card. Sometimes digital apps do not show the full policy details needed for an interstate claim.

Non-Local Witness Data. Local witnesses are easier to find later than visitors who might have been in the car with the other driver.

Having this information documented early makes the process of filing claims involving Out of State Drivers in Florida Accidents much smoother. It avoids the five costly mistakes to avoid after a crash that often ruin a strong case.

Modified Comparative Negligence and the 50 Percent Bar In 2023, Florida changed its negligence laws to follow a _Modified Comparative Negligence_ system. This means that if you are more than 50 percent")

In 2023, Florida changed its negligence laws to follow a "Modified Comparative Negligence" system. This means that if you are more than 50 percent at fault for the accident, you cannot recover any money from the other driver. This rule applies even if the visitor comes from a state with different negligence laws.

The visitor's insurance company may try to shift blame onto you to avoid paying, citing your unfamiliarity with their home state's driving habits. Staying focused on the crash facts is essential to keep your responsibility under 50%. This tactic is common in snowbird car accidents, where insurers claim the local driver was speeding or distracted. This is a common tactic in snowbird car crashes.

Can I sue someone in Florida if they live in another state?

Yes. Under Section 48.193, Florida courts have Personal Jurisdiction over any driver who causes an accident on our roads, regardless of where they live.

What happens if the out-of-state driver has no insurance?

You will rely on your own PIP for medical bills and your Uninsured Motorist Coverage for additional damages like pain and suffering or lost wages.

How does a rental car affect my injury claim?

Due to the Graves Amendment, you generally cannot sue the rental company. You must seek compensation from the driver's personal insurance or their supplemental rental car liability Florida policy.

Will my medical bills be paid the same way?

Your initial medical expenses are processed through your Florida PIP. Any costs above that are pursued through the visitor's Bodily Injury Liability coverage or your own secondary policies.

We have the technical knowledge to navigate the Florida Long Arm Statute and the patience to track down out-of-state insurance adjusters. We handle the investigation of out-of-state insurance policy limits and manage the service of process through the Secretary of State.

Serving clients in Largo, Tampa, and throughout Hillsborough and Pinellas Counties, we bridge the gap between Florida law and other state regulations, ensuring that every available dollar of coverage is pursued with local expertise and dedicated advocacy.

If you are ready to hold a negligent visitor accountable, visit our Tampa headquarters or connect with our team in Largo today.

Phone: (813) 395-5829

Address: 12002 Race Track Rd, Tampa, FL 33626

Email: info@carterinjurylaw.com

Website: https://www.carterinjurylaw.com/

Disclaimer: This article is for general informational purposes and does not form an attorney-client relationship. For help with any personal injury or criminal case, reach out to Carter Injury Law.

Rear-end accidents happen all the time on busy roads in Florida. Many drivers think that the car in the back is always to blame when a crash occurs. In Florida, the law usually says the driver behind is at fault. But new laws and certain evidence can change who is responsible. You need to file a claim within two years according to Florida law.

In 2023, the Florida Department of Highway Safety and Motor Vehicles reported more than 390,000 crashes. Many of these happened in crowded places like Hillsborough County. These accidents can lead to high medical bills and long-lasting pain for those hurt.

Florida has recently made an important change in the law called House Bill 837. This law affects how long you have to seek justice in Tampa. Now, you have two years to file a negligence claim. Before this change, you had four years.

On March 24, 2023, this law went into effect. It means that people who are hurt in an accident have less time to sue. You can't sue if you wait more than two years after the accident. Because of this shorter time frame, it's very important to quickly gather evidence for your case.

House Bill 837 also changed how Florida thinks about shared blame. Florida now has a system for modified comparative negligence. You can't get any money if you are found to be more than 50% at fault. Because of this change, it is even more important to look into your Tampa car accident.

Many rear-end crashes happen because a driver does not stop in time. Several things, like how drivers act and the road conditions, can cause these accidents.

Distracted Driving

Using a phone or texting takes your focus away for a few seconds. When driving fast on the highway, this makes it hard to notice when cars in front slow down. The National Highway Traffic Safety Administration says that distractions cause many deaths each year.

Tailgating

Driving too close to the car in front is against Florida law. Drivers should keep a safe distance at all times. If the car ahead stops quickly, there is no space to react.

Speeding

Driving too fast makes crashes worse. It also means cars need more space to stop. Going fast can change small accidents into big ones.

Impaired or Drunk Driving

Drugs and alcohol make it hard to react quickly. Drivers who are impaired often do not see traffic changes until it is too late.

Weather Conditions

Heavy rain and fog happen often in South Florida and Tampa. These weather conditions make it hard to see and make the roads slippery. Drivers need to slow down to stay safe in these situations.

Mechanical Failures

A crash is not always the driver’s fault. Old brake pads or flat tires can stop a car from braking. In these situations, a repair shop or the manufacturer might be responsible.

Even low-speed rear-end crashes cause serious physical harm. The sudden motion of the impact places extreme stress on the spine.

Whiplash and Neck Injuries

Whiplash occurs when the head snaps forward and backward rapidly. This motion damages the muscles and nerves in the cervical spine.

Spinal Cord Damage and Back Injuries

Rear end impacts often result in herniated discs and spinal fractures. These injuries may require surgery or long-term physical therapy.

Traumatic Brain Injuries and Concussions

A brain injury can happen even without a direct hit to the head. The rapid acceleration causes the brain to move inside the skull.

Soft Tissue Injuries

Ligament tears and muscle strains are very common in sudden collisions. These injuries often involve significant pain and limited mobility.

Broken Bones

Drivers often brace themselves against the steering wheel before impact. This can result in broken wrists, arms, or legs.

Many symptoms like neck stiffness or nerve pain do not appear immediately. These delayed symptoms make it vital to see a doctor right after a Tampa crash.

Also read: Can You File a Claim for Delayed Pain After a Car Accident in Florida?

Victims can seek money for financial losses and their personal suffering.

Economic Damages

These cover measurable costs like medical bills and lost wages. They also include the cost of vehicle repairs and future rehabilitation.

Non-Economic Damages

These compensate for pain, emotional distress, and reduced quality of life. Permanent disability also falls under this category.

Punitive Damages

Courts award these in rare cases of extreme negligence. Driving under the influence is a common reason for punitive damages.

Who Is at Fault in a Rear-End Collision in Florida")

While the rear driver often carries the blame, the "rebuttable presumption" can be overcome if the rear driver can prove the front driver acted negligently. Common exceptions include:

If the lead driver suddenly slams on the brakes for no reason in an unexpected place, like in the middle of a highway with no hazards.

If the brake lights on the front car weren't working, the driver behind it wouldn't have known that the car was slowing down.

If a driver cuts off another car suddenly, the driver in the back won't have time to react.

When the driver in front suddenly puts the car in reverse at a stoplight or in traffic.

If the rear driver's vehicle suffered a sudden, unexpected mechanical failure, such as total brake failure.

No, the rear driver is not always at fault in a rear-end collision in Florida. Florida law imposes a "rebuttable presumption" of negligence on the rear driver, meaning they are assumed to be at fault unless they can provide evidence to show the lead driver or another party was responsible.

The presumption that the rear driver is at fault stems from the legal requirement under Florida Statute 316.0895 to maintain a safe following distance. If a driver hits the car in front, it is typically assumed they were following too closely, distracted, speeding, or otherwise failed to control their vehicle.

When the Front Driver May Be at Fault")

The presumption of fault changes if the lead driver caused the danger. Common examples include:

Sudden and unjustified stops in the middle of a road.

Reversing unexpectedly into the car behind them.

Driving with malfunctioning or broken brake lights.

Making unsafe lane changes right in front of another car.

Stopping illegally in a moving lane of traffic.

Now, both drivers can be at fault under the new rule. A court decides how much blame each driver has.

Example:

Rear driver is 70% responsible.

Front driver is 30% responsible.

The rear driver can still get money, but it will be 70% less. If you are 51% at fault, you will not get anything. This is why it is very important to show what the other driver did wrong.

Evidence Needed to Challenge Fault")

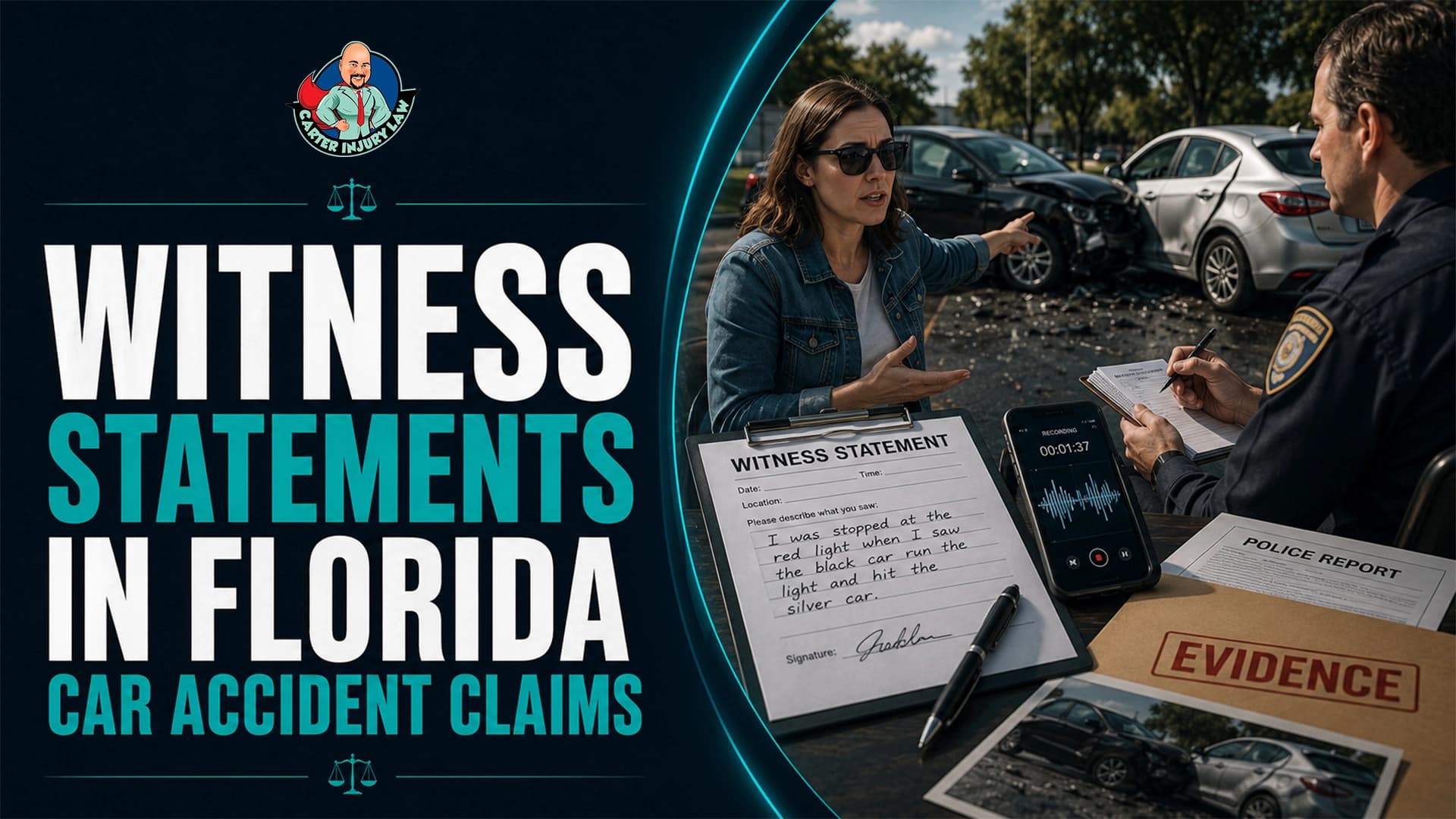

You need clear proof to show that the other driver was at fault. Carter Injury Law looks for important things to help your case:

Official documents from Hillsborough County law enforcement.

Statements from people who saw the crash happen.

Video evidence of the moments before the impact.

Information from the vehicle’s computer about speed and braking.

Professional analysis of skid marks and impact angles.

Call the police to ensure an official record exists.

Take photos of both vehicles and the surrounding road.

Get contact information from every witness at the scene.

Do not apologize or admit any fault to anyone.

Visit a doctor immediately to document your physical condition.

Also read: Five Costly Mistakes to Avoid After a Crash

If you were injured in a rear-end crash, Carter Injury Law is ready to help. Our team understands Tampa traffic laws and the new Florida statutes. Contact us today for a free confidential case evaluation about your accident.

How do insurance companies determine fault?

They review the police report and interview both drivers involved. They also inspect the damage to see which car hit which area.

What if multiple cars are in a chain reaction?

These cases are very complex. Each impact is analyzed to see which driver started the chain.

Can vehicle technology help my case?

Yes, dashcams and sensors provide objective proof of what happened. They often show if a lead driver stopped without cause.

Disclaimer: This article is for general informational purposes and does not form an attorney-client relationship. For help with any personal injury or criminal case, reach out to Carter Injury Law.

A quiet drive on a sunny afternoon in the Sunshine State can change in a heartbeat. The sound of screeching tires stays with you long after the dust settles. Once the sirens fade and you return home, a new challenge begins. You receive a call from a person who sounds professional and perhaps even kind. This person is the insurance adjuster.

We want you to understand the way professional agents analyze damage reports and medical costs after a wreck. Carter Injury Law sees how these interactions shape lives every day.The process of valuation is about what the insurance company can justify paying while keeping their profits high. They look at your medical records and the police report. Every piece of data fits into a larger puzzle. Knowledge is your best tool in this situation.

The foundation of any case starts with the insurance policy. An adjuster reviews the limits of the coverage first to know the maximum amount the company might have to pay. However, their goal is to keep the payout far below that limit. They look at the facts of the accident through a lens of risk. They ask if a jury would find their driver responsible and look for any reason to blame you for the impact.

We see adjusters start with a skeptical mindset. They treat every claim as a potential drain on company resources. This is simply their business model. They use standardized methods to ensure that every office follows the same rules. This makes the process feel cold and mechanical. However, we know how to work within that system to highlight the human side of your story.

The initial stages of a claim are often the most critical. Florida has unique laws that dictate how much money is available. The representative begins by looking at the basic requirements of your policy. They check if you followed all the rules from the very start.

The first thing an evaluator checks is the timeline of your medical treatment. They look for any reason to deny the claim before it even starts. Florida law is very strict about when you must seek help.

Florida saw 362,063 motor vehicle accidents in 2025 with 235,964 of those resulting in reported injuries.

Source: Florida Highway Safety and Motor Vehicles (FLHSMV)

If you wait too long to see a doctor, the company will claim your injuries did not happen in the crash. They specifically look for the PIP 14-day rule Florida compliance. This rule requires you to seek medical attention within two weeks of the accident to access your Personal Injury Protection benefits. If you miss this window, you lose a significant portion of your initial coverage.

Florida is a no-fault state. This means your own insurance usually pays for your initial medical bills. However, if your injuries are severe, you can step outside of this system to sue the at-fault driver.

The adjuster evaluates whether your case meets the Florida serious injury threshold. This legal standard requires proof of permanent injury or significant scarring. If the company decides your injury is minor, they will offer a very small amount of money. They hope you will accept it and walk away without a fight.

Even small choices, like what you say to an insurer, can influence the outcome of a case. You can read more in this overview of five costly mistakes drivers make after a Largo car accident.

How Insurance Software Calculates Florida Car Accident Settlements")

Many people believe a human being sits down and thinks about how much an injury is worth. In reality, modern insurance companies rely heavily on technology. Computer Programs and Data Points

Most large insurance companies use a specific type of program to handle their heavy lifting. The most famous one is known as Colossus insurance software. This program uses thousands of data points to create a settlement range.

The software assigns a value to every injury code in your medical file. However, a computer cannot understand how a neck injury prevents you from sleeping. We know that these programs often ignore the human element of suffering. The company uses the software output as their ceiling for negotiations. They rarely tell you that a machine made the decision for them.

Because software drives the process, the quality of your medical records is vital. If your doctor uses vague language, the software assigns a lower value. Adjusters look for specific value drivers in your files, such as specialist visits or MRI scans.

We advise our clients to be very thorough when describing their pain to doctors. This ensures the Florida car accident settlement process reflects the actual severity of the situation. Every word in those records becomes data for the insurance company algorithm.

Once the adjuster moves past the software, they look at the hard numbers. They divide your claim into two main categories: economic damages and non-economic damages. They use math to justify their final offer to their supervisors.

Economic damages are the easiest to calculate because they have a receipt. This includes your hospital bills and lost wages. However, recent changes in the law have made this more complex.

The Florida Transparency in Damages law changed how adjusters look at medical costs. They no longer care what the hospital billed you; they only look at what was actually paid by you or your health insurance.

Accident victims who hire an attorney receive settlements that are nearly 3.5 times higher on average than those who represent themselves.

Source: Insurance Research Council (IRC)

The hardest part of the evaluation is the non-economic damage. Companies often use the Multiplier method to find this number. They take your total medical bills and multiply them by a number between one and five. If your injury is life-changing, they use a higher number. If they think you will recover quickly, they use a lower one.

Recent Florida Laws That Impact Car Accident Injury Claims")

The legal landscape in Florida changed significantly in 2023. These changes give insurance companies more power than they had in the past. It is more important than ever to understand the current Florida personal injury claim evaluation factors.

Florida recently adopted a new standard for fault: the Florida comparative negligence 51% rule. Under this law, if a company can prove you were 51% at fault for the crash, you get nothing. The insurance company will search for any reason to blame you.

Certain roads develop accident patterns due to traffic volume and road design. You can learn more about this issue in “A Closer Look at the Frequent Accidents Along Ulmerton Road.”

The state reduced the time you have to file a lawsuit from four years down to two years. Adjusters know this well. They may use insurance adjuster tactics Florida car accident strategies to delay your claim. They might act like they are working on a settlement until the deadline passes. Once the two-year mark hits, your right to sue vanishes.

6)The Final Stages of Your Case

An insurance representative will not finalize a claim until they know the full extent of your injuries. They are waiting for a specific medical milestone to be sure that the case will not get more expensive later.

The company wants to see that you have reached Maximum Medical Improvement (MMI). This is the point where a doctor says you are as healthy as you are going to get. If you still have pain at this stage, it is considered a permanent injury. Adjusters wait for this report because it tells them there are no more surprise medical bills coming.

Medical Lien Coordination

Many people cannot afford treatment while they wait for a settlement. This is where a Letter of Protection (LOP) becomes important. This document allows you to get medical care now and pay the doctor later from your settlement money. Adjusters review these letters carefully to ensure treatment is necessary.

Why Insurance Companies Start With Low Settlement Offers")

When the evaluation is complete, the representative makes an offer. This offer is rarely their best number. It is a starting point for a long negotiation. They expect you to counter.

They hope a quick check will tempt you to sign away your rights. However, the average car accident settlement Florida victims receive is often much higher when they refuse that first low offer.

In a negligence action, any party found to be greater than 50 % at fault for his or her own harm may not recover any damages.

Source: The Florida Senate (Florida Statute 768.81)

The days following a car crash are filled with big decisions. You are dealing with pain, car repairs, and the stress of missing work. You do not have to carry the burden of the insurance claim by yourself. Learning how professional agents analyze damage reports and medical costs is the best way to protect your future.

We want to ensure that the insurance company treats your claim with the attention it deserves. If you have questions about your specific situation, reach out for a professional opinion at Carter Injury Law.

Address: 1234 Legal Way, Suite 100, Tampa, FL 33602

Phone: (813) 555-0199

Website: www.carterinjurylaw.com

Email: info@carterinjurylaw.com

Disclaimer: This article is for general informational purposes and does not form an attorney-client relationship. For help with any personal injury or criminal case, reach out to Carter Injury Law.

When you walk into a doctor’s office after a car crash or a slip and fall in Tampa, you aren't just there for a checkup. You are there to create the blueprint for your legal recovery. In the world of law, if it isn't in writing, it didn't happen. This is exactly why medical records in Florida injury cases serve as the most critical evidence you can provide. Your doctors' notes, test results, and discharge papers tell a story that an insurance company simply cannot ignore.

Many victims believe that their testimony—the simple truth of their pain—is enough to win a settlement. However, Florida is a "No-Fault" state with complex thresholds for pain and suffering. Without a paper trail, your words are just air. A strong Florida personal injury claim relies on objective, scientific proof that connects your accident to your physical limitations.

For any Florida personal injury claim, the burden of proof rests on your shoulders. You must show that your injuries are real, severe, and directly caused by the accident. Medical records act as an objective third-party witness. They bridge the gap between "my back hurts" and "there is a documented disc protrusion at L4-L5."

When an attorney looks at your file, they look for "causation." This is the link between the defendant's negligence and your specific injury. If you wait three weeks to see a doctor, that link weakens. The insurance adjuster will claim that you hurt your back while gardening or lifting groceries, not during the car accident.

Honesty is your best asset when you seek treatment. You should describe your symptoms clearly and mention every area of your body that feels "off." Often, victims experience neck or back pain days after a car accident rather than immediately. This delayed onset is common with soft tissue injuries and whiplash.

If you fail to mention a dull ache in your neck during your first visit, the insurance adjuster may argue that the injury occurred later. Be thorough and specific about how your life has changed since the incident. According to the Florida Bar’s consumer guidelines, documenting the impact on your daily routine is essential for a successful outcome.

Do not just say it hurts; describe if it is sharp, dull, or radiating.

Tell the doctor if you can no longer lift your child or drive to work.

Ensure the story you tell the paramedic matches the story you tell the specialist.

If the accident caused anxiety or PTSD, ensure these symptoms are noted.

Why Should You Avoid a Gap in Your Treatment_")

Consistency is the secret sauce of a successful case. If a doctor prescribes physical therapy twice a week, you must go twice a week. If you skip appointments, you send a signal to the insurance company that you are either healed or not seriously hurt. This logic applies to every type of incident, whether you are exploring legal avenues after a bus accident or a simple fender-bender in Tampa.

A "gap in treatment" is the first thing an adjuster looks for to devalue your settlement. They use these gaps to argue that your Florida personal injury claim is exaggerated. Even if your life is busy, your health and your legal case must remain a priority. Medical records in Florida injury cases that show a steady, unbroken line of treatment are much harder to dispute in a courtroom.

Insurance companies use sophisticated software to analyze your records and assign a "value" to your pain. They look at your medical records in injury cases to see if you followed medical advice and if the costs align with typical local rates. Under Florida Statute 90.803(4), medical statements made for diagnosis or treatment are considered highly reliable in court.

Adjusters will also look for "pre-existing conditions." If you had a back injury ten years ago, they will try to blame your current pain on that old issue. However, Florida law allows you to recover damages for the aggravation of a prior condition. Your new records must clearly show how the accident made your old injury worse. This is a nuance often seen in comparative negligence in bicycle accident cases, where every detail of the victim's history is scrutinized.

To ensure your medical records are complete, your attorney will need to gather a mountain of paperwork. You should keep a folder of everything you receive from the moment of the crash.

Emergency room records establish the "immediate" nature of your injuries and creates the first link in the chain.

X-rays, MRIs, and CT scans provide undeniable visual proof of harm that a jury can see.

Notes from neurologists or orthopedic surgeons carry more weight than a general practitioner.

A history of prescribed painkillers or muscle relaxants proves the severity of your discomfort.

How Does Florida Law Handle Medical Privacy_")

While your health information is private under HIPAA, filing a personal injury claim means you must share relevant records with the opposing side. This does not mean they get to see everything you have ever discussed with a doctor. A skilled lawyer ensures that the defense only sees what they are legally entitled to see.

In Tampa, judges are strict about "discovery" rules. We work to protect your privacy while ensuring that the medical records that support your claim are front and center. This balance is vital for maintaining your dignity while fighting for the money you deserve.

Yes. If you tell your chiropractor that your neck is an 8/10 on the pain scale, but you tell your primary doctor it feels "fine," you have created a conflict. Defense attorneys love these contradictions. They will use them to paint you as untrustworthy.

When you are involved in an injury claim, every medical professional you see is, in a sense, a witness. Ensure that your descriptions are honest and consistent across the board. If a symptom improves, say so. If a new pain develops, report it immediately. The goal of medical records is to provide a transparent, accurate timeline of your path to recovery.

Standard medical charts are often filled with shorthand and codes. To a jury, these can be confusing. A "narrative report" is a document where your doctor explains in plain English what happened to you. They will state their opinion on whether your injury is permanent and what your future medical needs will look like.

Future medical costs are a massive part of a Florida personal injury claim. If you will need surgery in five years, or if you will require lifelong medication, your current medical records must reflect that. Without a doctor’s written forecast, you cannot ask for money to cover future bills.

Trust Your Case to a Local Tampa Expert")

It's hard to get better while also dealing with the healthcare system. We take that weight off your shoulders at Carter Injury Law. We know which Tampa hospitals take a long time to process paperwork and how to get the diagnostic images we need to support your case.

David Carter and our dedicated team understand the specific nuances of the Tampa Bay legal landscape. Whether you were hurt on a busy highway like I-275 or in a local neighborhood, we fight to ensure the insurance companies treat your Florida personal injury claim with the respect it deserves.

We offer a free, no-obligation case review to help you understand what your records are worth. Let us handle the legal heavy lifting so you can focus on getting your life back to normal.

Call us 24/7 at (813) 922-0228 or message us directly to get started. Your recovery starts with the right evidence and the right team.

You are stuck in traffic on a busy road in Florida. At a red light, the car behind you hits your bumper. You get out and see that the trunk is not dented. This event doesn't seem very important or memorable. However, many people suffer from a low-impact car accident in Florida that causes long-term physical pain.

You might think that a lack of metal damage means your body is safe. This is a common mistake that many drivers make after a small bump. The impact forces do not disappear just because the plastic bumper looks fine. These forces move through the car frame and into your seat.

A car is a heavy machine made of steel and plastic. When two machines collide, energy must go somewhere. Modern cars use plastic covers to hide the actual safety bars. These covers often pop back into place after a hit. This makes the car look undamaged to the naked eye.

However, the energy of the hit travels deep into the vehicle structure. This energy eventually reaches the human occupants. You feel the jolt in your neck and your lower back. This energy transfer happens in a fraction of a second.

Many people experience a vehicle wreck in the sunshine state while they are stopped at a light. The surprise of the hit makes the injury worse. Your muscles are relaxed and they cannot protect your joints.

Plastic is flexible and resilient. It can take a hit and return to its original shape. This is great for the resale value of your car. It is bad for your personal health. You might look at the rear of your car and see zero property damage after a tap. This leads you to tell the other driver that you are okay.

You might even decide not to call the police. However, the internal parts of the bumper may be crushed. More importantly, your spinal discs may have shifted. We see clients every week who ignored a small tap only to regret it later.

“Experimental results from low speed rear end collisions, which involved live human subjects, have shown that the peak head acceleration is at least two and a half times larger than peak acceleration of the struck vehicle.”

Source: Florida Atlantic University (FAU) College of Engineering

Medical Reality of Invisible Harm")

Your body is much more fragile than a car. A piece of steel can take a lot of pressure before it bends. Your neck and back rely on tiny ligaments and tendons to stay stable. A small jolt can tear these tissues. These tears are too small for a standard X-ray to find.

You might feel a little stiff on the day of the crash. You assume the stiffness will go away with some rest. However, the pain often grows over the next forty-eight hours. This is why legal claims for collisions are so complex. The injury is real but it is hard to see.

Even if your car shows little damage, symptoms may appear later, which we break down in Neck or Back Pain Days After a Car Accident? What It Means Under Florida Law

Whiplash is the most frequent injury in a low-speed crash. It happens when your head snaps forward and back. This motion stretches the muscles beyond their normal limit. You might feel a headache or a dull ache in your shoulders. These are signs that your body is in distress.

You should seek medical treatment as soon as possible. A doctor can check for nerve damage or disc issues. If you wait too long, the insurance company will say you were not hurt in the crash. They will claim you got hurt somewhere else.

Some injuries do not show up for weeks. A small tear in a disc can leak fluid slowly. This fluid eventually touches a nerve. Then you feel a sharp pain down your arm or leg. We call this a soft tissue injury because it involves the flexible parts of your neck.

“Neck sprain or strain is the most serious injury in one-third of insurance claims for injuries in all kinds of crashes.”

Source: Insurance Institute for Highway Safety (IIHS)

Insurance firms are businesses. They want to keep their money. They use a very specific plan to fight small claims. They look at the repair estimate for your car. If the bill is under two thousand dollars, they flag the file. They call these MIST cases. This stands for Minor Impact Soft Tissue. They assume that low damage equals low injury.

However, science proves this assumption is wrong. You need an advocate to fight this visual bias. We show the jury that your body is not made of plastic.

Adjusters love to show photos of a clean bumper to a jury. They want the jury to think you are lying about your pain. They ignore the medical records and the expert testimony. They focus only on the car. However, insurance companies know the truth about energy transfer.

They just choose to ignore it to save money. They hope you will get frustrated and quit. They hope you will take a tiny settlement and sign a release. Once you sign that paper, you can never ask for more money.

A friendly adjuster might call you the day after the crash. They will ask how you feel. They also use software to decide what your case is worth. This software does not care about your daily pain. It only cares about the cost of the medical bills you have paid. We help you talk to these adjusters so you do not hurt your case.

“More than 235,964 motor vehicle crashes in Florida involved reported injuries in 2025.”

Source: Florida Department of Highway Safety and Motor Vehicles (FLHSMV)

Legal Standards Under Florida Statutes")

The law in our state is unique. We follow a no-fault system. This means your own insurance pays for your initial care. This is known as personal injury protection pip coverage. It covers 80% of your medical costs up to ten thousand dollars.

However, there are many rules you must follow. If you miss a deadline, you lose your money. You must understand how Florida law works to get the most from your policy. We guide you through every step of this confusing process.

You must see a doctor within 14 days of the crash. If you wait until day fifteen, your insurance will pay zero dollars. This rule is very strict. This is why seeking medical care is your top priority. Your PIP also pays for 60% of your lost wages if you cannot work. We make sure the insurance company sends your checks on time.

You cannot sue the other driver for pain and suffering unless your injury is permanent. This is a high bar to reach. You need a doctor to state that you will never fully recover. We work with medical experts to prove this fact.

If we can prove a permanent injury, we can pursue a claim against the at fault driver for more money. This money covers the pain you feel every day. It covers the loss of your quality of life. We do not stop until we find every available dollar for your recovery.

What you do after a crash matters. You must act with a plan. First, you should call law enforcement to the scene. A police report is a vital piece of evidence. It shows who was at fault and what happened. Second, you must take photos of both cars.

Do not just take photos of the damage. Take photos of the lack of damage too. This helps us explain the physics of the hit later. Third, you must never apologize at the scene. An apology can be used as an admission of fault.

Many drivers unknowingly damage their own claims in the hours after a collision, which is why we explain common errors in Five Costly Mistakes to Avoid After a Crash, According to a Largo Auto Accident Lawyer.

Keep a folder for every paper you get. This includes the exchange of information and your medical discharge papers. Write down the names of any witnesses. If someone saw the other driver on a phone, that is huge for your case.

We use this evidence to fight modified comparative negligence arguments. The other side will try to say the crash was your fault. We use the evidence to prove they are wrong. Your focus should stay on your physical recovery while we handle the data.

You should not sign anything without a lawyer. The insurance company might offer you a few hundred dollars right away. This is a trick to get you to close the case. Talk to a professional first. We handle accidents in Florida every single day. We know the courts and we know the adjusters.

If you need professional legal guidance after an accident, you can reach out to Carter Injury Law, PA for a free consultation. We are committed to treating every client like family and fighting for the compensation you deserve.

Phone: (813) 922-0228

Address: 3114 N Boulevard, Tampa, FL 33603

Website: www.carterinjurylaw.com

Disclaimer: This article is for general informational purposes and does not form an attorney-client relationship. For help with any personal injury case, reach out to Carter Injury Law.

People know Florida for its beaches and theme parks, but its roads tell a different story. Traffic is a way of life here, as you know if you've ever been stuck on I-4 or the Howard Frankland Bridge. Sadly, when there is a lot of traffic, there is a high risk of accidents. It’s important to know how the law works after a crash, which is why Carter Injury Law has provided this guide on Florida auto accident laws explained for injured drivers.

Florida's laws are different from those of many other states. Because Florida is a no fault state, the process for seeking compensation begins with your own insurance provider, regardless of who caused the wreck. However, this does not mean the person who hit you is off the hook.

One of the most common points of confusion for residents in Largo and Tampa is the phrase "florida is a no fault state." This does not mean that no one is to blame for the crash. Instead, it refers to how your initial medical bills are paid.

Under this system, your own insurance provider is responsible for paying a portion of your medical costs and lost wages regardless of who caused the accident. This is handled through a specific type of coverage that florida law requires every driver to carry.

The backbone of the no-fault system is personal injury protection pip. This coverage is mandatory for all motor vehicle owners in Florida. Here is what you need to know about your PIP benefits:

Standard PIP policies provide up to $10,000 in benefits.

PIP typically pays 80% of your medical expenses, such as ER visits, surgeries, and physical therapy.

If you cannot work, PIP pays 60% of your lost income.

If the worst happens, PIP provides a $5,000 death benefit for funeral costs.

It’s important to note the "14-Day Rule." To qualify for PIP benefits, you must seek medical treatment within 14 days of the accident. If you wait longer, the insurance company can legally deny your claim. Furthermore, if a doctor does not determine that you have an "Emergency Medical Condition" (EMC) as defined by Florida Statutes Section 627.732, your PIP benefits may be capped at a mere $2,500.

What Are the Current Florida Auto Insurance Requirements_")

To legally operate a vehicle in Florida, you must meet specific insurance requirements. These laws are in place to ensure that there is at least a baseline of financial protection on the road. However, many drivers are surprised to learn that Florida's minimum requirements are among the lowest in the nation.

Currently, the state requires:

$10,000 in Personal Injury Protection (PIP)

$10,000 in Property Damage Liability (PDL)

Interestingly, Florida does not technically require "Bodily Injury Liability" (BIL) for most private passenger vehicles. This means that the person who hit you might not have any insurance to pay for your long-term care or pain and suffering emotional distress. This is why we always recommend that our clients purchase Uninsured/Underinsured Motorist (UM) coverage to protect themselves from drivers who only carry the bare minimum.

If you were involved in a collision with an unconventional vehicle, the rules might differ slightly. For instance, you can learn more about how liability works when a golf cart vs. a car collide in residential neighborhoods.

Following a collision, your first priority is safety, but your second should be documentation. Under Florida Statutes Section 316.066 drivers must report any accident involving injuries, death, or property damage estimated at $500 or more to law enforcement immediately.

When an officer arrives, they will create an official crash report. This document is a cornerstone of your personal injury claim. It contains:

The date, time, and precise location of the incident.

Identification of all parties and vehicles involved.

The officer's initial assessment of how the crash happened.

Whether any citations were issued for traffic violations.

You can typically obtain a copy of this report through the FLHSMV Crash Portal. Remember, while the report itself might not always be admissible as evidence in a trial due to "accident report privilege," the information within it helps your attorney track down witnesses and preserve physical evidence before it disappears.

Does Your Injury Qualify as a Permanent Injury_")

Because of the no-fault system, you cannot usually sue the other driver for non-economic damages unless your injuries are severe. To "step outside" the no-fault system and seek compensation for pain and suffering emotional distress, you must prove that you sustained a permanent injury.

According to the florida statutes, a permanent injury is generally defined as:

Significant and permanent loss of an important bodily function.

A permanent injury within a reasonable degree of medical probability.

Significant and permanent scarring or disfigurement.

Death.

Expert medical testimony and a thorough understanding of medical record presentation are necessary to prove this threshold. You are probably only eligible for the benefits of your PIP policy and any property damage coverage the other driver may have if it is anticipated that your injury will heal completely over time.

One of the most significant changes to florida law requires your attention: the statute of limitations. For many years, injured drivers had four years to file a lawsuit. However, as of March 2023, the time limit for most negligence-based personal injury cases has been slashed.

How Long Do You Have to File a Lawsuit?

Two-Year Limit: For accidents occurring on or after March 24, 2023, the statute of limitations is now only two years from the date of the crash.

Four-Year Limit: Only if your accident occurred before March 24, 2023, do you still have the old four-year window.

Government Claims: If you are hit by a city or state vehicle, there are even shorter notice requirements that must be met before you can sue.

If you miss this deadline, you lose your right to seek compensation forever. This is why it is vital to contact a lawyer early in the process. You can find more details on how personal injury settlements are paid out once the legal hurdles are cleared.

Another major shift in the law involves how we calculate fault. Florida recently moved from a "pure" comparative fault system to a "modified" one. This change has a massive impact on your ability to recover money if you were partially responsible for the accident.

Under the old rules, if you were 90% at fault, you could still recover 10% of your damages. Under the new rules, if you are found to be more than 50% at fault, you recover zero.

The insurance company will work tirelessly to shift the blame onto you. They might argue that you were speeding, distracted by your phone, or failed to use a turn signal. Their goal is to push your percentage of fault above that 50% mark so they can walk away without paying a dime.

This strict standard makes it more important than ever to have a legal team that can investigate the crash, gather dashcam footage, and interview witnesses to prove the other person was the primary fault driver. This is especially true for vulnerable road users, such as those discussed in our post about bicycle accident laws in Largo.

What Can You Recover in a Personal Injury Claim_")

If you meet the permanent injury threshold and the other driver is at fault, you can seek damages beyond what PIP covers. A comprehensive car accident claim seeks to "make the victim whole" by covering both economic and non-economic losses.

Your claim may include:

Full medical expenses include the 20% that PIP did not pay, plus all future medical costs for surgeries or therapy.

Total Lost Income can recover the 40% of wages PIP missed, plus any future loss of earning capacity.

Trauma and injury make up for the physical strain, emotional distress, and pain that the trauma has caused.

The cost to repair or replace your vehicle and any personal items inside.

Managing these details while trying to heal is an immense burden. Avoiding common mistakes after a crash is the first step toward securing the settlement you deserve.

We know that a car accident is more than just a legal document; it changes your life. We are based in Tampa and serve clients all over Florida, including Largo and the Hillsborough and Pinellas counties that are close by.

David J. Carter and our hard-working team have a reputation for being strong advocates against big insurance companies. We know how they try to make your personal injury claim worth less, and we won't back down. We make sure that you are never just a case number by giving each car accident claim a personal touch.

We work on a contingency fee basis, meaning you pay nothing upfront.

As a fifth-generation Floridian, David Carter knows the local courts and the unique risks of Florida roads.

We assist with everything from finding the right doctors for your medical expenses to recovering your lost income.

You’ve got enough on your plate right now—let Carter Injury Law handle the rest from our Tampa office at 3114 N Boulevard. If you’re in Hillsborough County, give us a shout at (813) 922-0228, or call our Pinellas team at (727) 955-1922. We’re here to look out for you from day one.

Many people walk away from a crash scene feeling lucky because they do not have a scratch on them. However, you might wonder, can you file a claim for delayed pain after a car accident in Florida? The answer is a clear yes. It is very common for symptoms to wait a few days or even weeks to show up.

When this happens, you are still entitled to seek compensation. However, the legal process in Florida has very specific rules that you must follow to protect your rights. Dealing with a car accident is stressful enough without having to worry about hidden injuries that surface later.

From our home base in Tampa to the surrounding communities of Largo, Pinellas, and Hillsborough Counties, Carter Injury Law provides statewide advocacy for Floridians facing delayed injury symptoms.

When a collision occurs, your body enters a state of high alert. It produces a massive amount of adrenaline and endorphins. This is often called the fight-or-flight response. These chemicals act as natural painkillers. They can easily mask the pain of serious injuries for several hours or even days.

Once the adrenaline wears off and your body begins to relax, the delayed injuries become noticeable. You might wake up 3 days later and realize you can barely move your neck. This delay is a biological reality, and something urges you to get the help you need. Insurance companies know this happens, yet they often use the delay as a reason to question the validity of your situation.

Not every injury is as obvious as a broken bone. Many of the most common issues after a crash are internal or involve nerves and muscles in your body.

A very common issue for accident victims is whiplash. This happens when the head is jerked forward and back suddenly. This motion causes soft tissue injuries in the neck and upper back. It often starts as a dull ache and turns into sharp pain in your arms.

A traumatic brain injury can be extremely subtle. You do not have to hit your head on the dashboard to suffer a concussion. The jarring movement of the brain inside the skull is enough. Symptoms like headaches, dizziness, blurred vision, or mood swings might not be obvious right away. According to data from the Centers for Disease Control and Prevention, symptoms of a brain injury can evolve over time and may not be fully realized for days after the initial impact.

This is perhaps the most dangerous type of delayed pain. Deep bruising or internal bleeding can happen because of the pressure from a seatbelt. If you feel abdominal pain or see deep purple bruising days later, it is a medical emergency. These issues require an immediate medical evaluation to ensure your safety.

Florida 14 Day Rule for Medical Treatment After a Crash")

Florida has a very strict law regarding how long you can wait to see a doctor. This is known as the 14-day rule. Under Florida Statute section 627.736, you must seek initial medical care within 14 days of the accident to use your Personal Injury Protection or PIP benefits. If you wait until day 15 because your pain was delayed, you might lose your right to this coverage entirely.

According to the Florida Highway Safety and Motor Vehicles dashboard, there are hundreds of thousands of crashes in the state every year. Many people lose out on their benefits because they simply do not know about this 2-week window. Even if you think the pain is minor, you should seek medical attention as soon as possible to preserve your legal options.

Even if you make it to the doctor within 14 days, there is another hurdle in Florida. To access your full $10,000 in PIP benefits, a medical professional must determine that you have an Emergency Medical Condition or EMC. If the doctor decides your injury does not meet this specific legal threshold, your insurance coverage is capped at way less than full coverage.

This is a significant gap in coverage, especially if you have lost wages or need ongoing physical therapy. Finding a doctor who understands how to document these conditions is a major part of the recovery process.

Challenges With Insurance Claims for Delayed Car Accident Pain")

When you file a claim for an injury that did not show up immediately, the insurance company will likely be skeptical. Their goal is to pay out as little as possible.

They often use the "gap in treatment" argument. They will claim that if you were really hurt, you would have gone to the hospital right away.

They might even try to blame your pain on a preexisting condition rather than the crash. This is why having detailed medical records is so important.

You need to show a clear timeline of how the pain started and how it progressed. Without a strong legal advocate, it is easy to feel pressured into accepting a low settlement offer.

Also, you should avoid making these five costly mistakes to avoid after a crash that often ruin a strong case.

If you start feeling discomfort a few days after being hit by a careless driver, you need to act quickly. Do not ignore the signals your body is sending you.

Go to a doctor immediately for a full checkup. Tell them you were in a car accident so they know what to look for.

Be very specific with the doctor about every symptom, even the small ones.

Start a daily journal. Write down when the pain started and how it affects your ability to work or care for your family.

Keep copies of all your bills and discharge papers.

Do not sign anything from an insurance adjuster until you have spoken with a professional. Following these steps ensures that your delayed injury claims are backed by solid evidence.

How We Help Clients Maximize Compensation for Delayed Injuries")

We know that your injuries are real, even if they didn't appear on day one. Our team of personal injury attorneys works tirelessly to connect the dots between the accident and your current physical state.

If you are wondering about the statute of limitations for personal injury claims in Florida, you should know that the laws recently changed. You now have a shorter window to file a lawsuit than in years past. This makes it even more important to find a car accident lawyer who can guide you through the process. Whether you are dealing with neck or back pain days after a car accident, we are here to provide the support and local expertise you deserve.

We have seen thousands of cases where the most serious symptoms were the ones that took the longest to appear. It is our priority to get you the full value of your insurance claims while dealing with delayed pain. You need someone who will fight for the maximum compensation available for your specific situation.

Yes, as long as you seek medical treatment within 14 days of the accident, you are generally eligible for PIP benefits in Florida. However, if you wait until the 15th day, you will likely be denied coverage under your own policy.

You do not have to go to the ER, but you must see a qualified medical provider such as a doctor, chiropractor, or dentist. To get the full $10,000 PIP limit, you will need an Emergency Medical Condition diagnosis.

For accidents occurring after March 2023, the statute of limitations for negligence in Florida is generally two years. It is best to consult with a lawyer early to ensure you do not miss any deadlines.

According to NHTSA data, rear-end collisions are one of the leading causes of whiplash and other injuries that often have a delayed onset. These numbers highlight how common these "hidden" injuries really are across the United States.

Our team, led by David Carter and Rob Johnson, is dedicated to uncovering the truth behind your injuries and fighting for the justice you deserve. We handle the complex investigations and aggressive negotiations so that you can focus on getting back to your normal life.

If you are facing any delayed pain after a car accident, reach out to our team immediately.

Phone: (813) 395-5829

Address: 12002 Race Track Rd, Tampa, FL 33626

Email: info@carterinjurylaw.com

Website: https://www.carterinjurylaw.com/

Disclaimer: This article is for general informational purposes and does not form an attorney-client relationship. For help with any personal injury case, reach out to Carter Injury Law.

It's not often relaxing to drive through Tampa. There are risks everywhere, whether you're trying to get through the heavy traffic on I-275 during the morning rush hour or across the Howard Frankland Bridge at sunset.

When you call Carter Injury Law, you're not just getting someone to fill out forms. You are hiring a strategist. An experienced Tampa car accident lawyer evaluates every potential case through a specialized lens, looking for specific criteria that determine whether a claim will stand up against aggressive insurance adjusters or a jury.

But what exactly are they looking for? From the details in a police report to the nuances of Florida law, the evaluation process is both an art and a science.

The first thing any personal injury lawyer will explain is how Florida’s no-fault insurance system dictates the early stages of your recovery. Under this system, regardless of who caused the wreck, your own insurance provider is responsible for paying a portion of your medical bills and lost wages through Personal Injury Protection (PIP).

However, PIP has strict limits—usually topping out at $10,000. In a serious collision near Downtown Tampa or Ybor City, those funds can vanish before you even leave the emergency room. To step outside the no-fault system and pursue a car accident claim against the other driver, your injuries must meet a certain "permanency threshold."

Does the injury affect a major bodily function?

Is there a reasonable degree of medical probability that the injury will not heal?

Is the physical damage visible and lasting?

In the most tragic cases, families may pursue a wrongful death claim.

If your injuries are deemed "minor," you might be stuck with only your PIP benefits. An attorney will look at your initial diagnosis to see if your case has the "legs" to go after the at-fault party for full compensation.

While a police report is not always admissible as evidence in a Florida courtroom due to the "accident report privilege," it is the "North Star" for an initial case evaluation. When an officer from the Tampa Police Department or the Florida Highway Patrol arrives at the scene, they create a document that serves as the foundation for the entire investigation.

An attorney looks for a few important things in this report:

Was the other driver ticketed for a violation like running a red light or failure to yield?

How does the officer describe the point of impact and vehicle positioning?

Are there neutral third parties listed who can corroborate your version of events?

Do the sketches of the scene suggest a high-velocity impact consistent with your injuries?

If the report clearly places fault on the other driver, your personal injury claim becomes much stronger. However, even if the report is "neutral," an experienced firm knows how to dig deeper to find the truth.

What Are the Most Common Causes of Car Accidents in Tampa_ (2)")

To win a case, you must prove negligence. This means showing that the other driver failed to exercise "reasonable care." In our local area, common causes of car accidents often fall into predictable patterns. Negligence can take many forms, like a tourist who doesn't know how to get around the one-way streets in Downtown or a commuter who runs a yellow light on Brandon Blvd.

In 2026, distracted driving remains one of the top hurdles for road safety. It’s texting, using GPS, eating, or even interacting with complex infotainment systems. If an attorney can prove the other driver was distracted, it significantly increases the value of your case. We look for evidence like:

Cell phone records that show data usage at the exact time of the crash.

Witness statements describing the driver looking down at their lap.

Lack of skid marks, which suggests the driver never even hit the brakes because they weren't looking at the road.

Beyond distractions, we see many cases involving speeding, impaired driving, and aggressive lane changes. If you were involved in a more complex situation, such as a multi-car collision in Florida, the evaluation becomes even more granular to determine the "chain of events" that led to the first impact.

You cannot have a personal injury claim without an injury. While this sounds obvious, the "proof" is entirely dependent on your medical record. Insurance companies are notorious for claiming that an accident victim is exaggerating their pain or that their back problems were "pre-existing."

An experienced Tampa car accident lawyer will carefully review your charts to ensure there is a clear "causal link" between the crash and your physical condition. This is why we always tell clients, "Do not skip your doctor appointments."

Your medical expenses are the most tangible part of your "damages." This includes more than just the first hospital bill; it covers:

Ambulance and emergency room fees.

Surgeries and follow-up specialist visits.

Physical therapy and chiropractic care.

Prescription medications and medical devices (like braces or crutches).

When evaluating a case, we look at whether the treatment is "reasonable and necessary." If you waited three weeks to see a doctor after a crash near Busch Gardens, the insurance company will argue you weren't actually hurt. Immediate and consistent documentation is the key to a successful settlement.

A lawyer who simply waits for the insurance company to send a check is doing you a disservice. A proactive attorney gathers evidence immediately. Evidence is "perishable"—skid marks wash away in the Florida rain, and surveillance footage from a local gas station might be overwritten in 48 hours.

When we evaluate a case, we look for:

Did a nearby Ring camera or a Tesla’s dashcam capture the impact?

Do we need an accident reconstructionist to prove the speed of the other vehicle?

Are there vehicle parts or "black box" data that prove mechanical failure or driver error?

Sometimes, the "vehicles" involved aren't even cars. We’ve seen unique cases like a golf cart vs car accident, where the rules of the road and insurance coverage can get incredibly murky. A professional who knows where to look for the "missing pieces" can change the whole course of your claim.

Does Your Case Meet the Statute of Limitations Deadline_")

This is perhaps the most critical part of a modern evaluation. Following the massive legal overhaul in March 2023, the statute of limitations for negligence-based claims in Florida was cut in half.

Important Note: For any accident occurring on or after March 24, 2023, you now have only two years to file a lawsuit. Under the old florida law, victims had four years.

In 2026, we are seeing many accident victims who waited too long to call a lawyer, only to find out their right to sue has expired. If you wait until the 23rd month to start your car accident claim, you are leaving your attorney very little time to investigate and negotiate. Speed is now a legal necessity.

Most car accident cases never see the inside of a courtroom. Instead, they end in a settlement. But how do you know if an offer is fair? Personal injury attorneys use a variety of factors to determine the "true value" of a case. They don't just look at the bills you have today; they look at the long-term impact.

If you have suffered a traumatic brain injury or a spinal cord issue, your needs will extend for years. We calculate:

Will you need another surgery in five years?

Can you still perform the same job you had before the accident?

How has your quality of life diminished?

If an insurance company offers a "quick check" just days after a crash, it is almost certainly a lowball offer. An experienced lawyer will compare that offer against the total "economic and non-economic" damages to ensure you aren't leaving money on the table. For more on this, check out our guide on how to maximize car accident compensation.

One of the biggest myths about hiring a car accident lawyer is that it is too expensive. The reality is that most reputable firms work on a contingency fee basis. This means you pay $0 upfront. The attorney only gets paid if they successfully recover money for you.

This "no-win, no-fee" structure is a huge advantage for accident victims who are already struggling with medical bills and missed work. It also ensures that your lawyer is highly motivated to get the best possible result. During your free consultation, a lawyer will explain exactly how the percentage works, so there are never any surprises at the end of your case.

A free consultation is a two-way street. While the lawyer is evaluating your case, you should be evaluating the lawyer. You want to ensure you are getting legal representation that is communicative, experienced, and local to Tampa.

When you sit down with us, we will ask:

What happened in the moments leading up to the impact?

Where have you gone for medical treatment so far?

Has any insurance adjuster tried to record a statement from you?

How has the injury affected your daily life and family?

We want to understand the human side of the story. Whether you were injured at work in Florida or while running errands in Westchase, your story matters.

Why Choose an Experienced Tampa Car Accident Lawyer from Carter Injury Law_")

We know that every personal injury claim is about someone trying to get their life back on track. Because we have deep roots in the Tampa area, we have an advantage when it comes to dealing with local courts and knowing the dangers of our roads.

Our firm handles a wide range of negligence cases, including:

Complex Auto Crashes Including rideshare and commercial vehicle accidents.

Delivery truck accidents, which often involve federal safety regulations.

Medical malpractice, when a healthcare provider makes a catastrophic error.

Premises liability, such as slip and fall incidents at local businesses.

Wrongful death for families who have lost everything.

We know how stressful the legal situation will be in 2026. With the shorter statute of limitations and the new "modified comparative negligence" rules (where you can't get anything if you're more than 50% at fault), it's more important than ever to have a strong lawyer on your side. If you want to learn more about how to use Florida's legal system, check out the Florida Bar's consumer resources.

Let Carter Injury Law do the heavy lifting from our Tampa office at 3114 N Boulevard. We will carefully read the police report, look over every part of your medical record, and fight with the insurance companies so you can focus on getting better.

Call us at (813) 922-0228 if you live in Hillsborough County or the area around it. If you live in Pinellas County, call our team at (727) 955-1922 to make sure your rights are protected from the start.

If you live in Largo, you know the feeling. You’re driving down East Bay Drive on a Tuesday afternoon, just trying to get home or maybe heading to the grocery store. Suddenly, traffic starts to slow down. You see the blue and red lights flashing ahead.

My heart always sinks a little when I see that. As an injury lawyer, I know what those lights usually mean. But as a neighbor and a member of this community, my stomach really drops when I see a teenager standing by the side of the road, looking terrified, phone in hand, staring at a crumpled bumper.

Teen driver accidents in Largo aren’t just a statistic on a government spreadsheet. They are happening right here, at the intersections we drive every day. I’ve had countless parents sit in my office, still shaking from the call they got an hour prior. They are worried about their child’s health, obviously. But once the dust settles, a new worry sets in. They start asking the hard questions about money, lawsuits, and their family’s future.

I want to have a frank conversation with you today. We need to talk about why our kids are crashing and the scary reality of who actually pays the price when they do.

People ask me all the time, "David, are drivers getting worse?" Honestly? It’s a mix of things. But for teenagers specifically, driving in Pinellas County is like being thrown into the deep end of the pool before you know how to tread water.

There are real reasons why we are seeing an uptick in crashes involving young drivers.

The "Conflict Points" Are Everywhere

Largo isn’t a sleepy town anymore. We have heavy commercial traffic mixing with residential neighborhoods.

Have you driven on U.S. 19 or near the Gateway Expressway project lately? It’s confusing enough for me, and I’ve been driving for decades. For a 16-year-old with six months of experience, shifting lanes, concrete barriers, and sudden stops are a recipe for disaster.

Places like Ulmerton Road and Seminole Boulevard are notorious. You have cars trying to beat yellow lights, people making U-turns, and tourists who don’t know where they’re going. These are "conflict points." An experienced driver knows to hover over the brake pedal here. A teen driver usually assumes the coast is clear until it’s too late.

The "100 Deadliest Days"

We hear this term in the safety industry, but it plays out consistently in Florida. The period between Memorial Day and Labor Day is dangerous. School is out. Teens aren’t driving to class; they are driving to the beach. They are driving to friends' houses. They are on the road later at night.

In Largo, this often means more kids in the car. And that is a huge factor. When a teen driver has two or three friends in the passenger seats, the risk of a fatal crash doubles. It’s simply too much distraction inside the vehicle to handle the chaos outside the vehicle.

Tech Is a Double-Edged Sword

We all know about texting. We hammer that into our kids’ heads. Don’t text and drive.

But the cases I’m seeing now involve different kinds of distractions.

GPS Apps: a kid looking down to see which turn to take for that new restaurant.

Streaming Music: trying to find a specific playlist on Spotify while merging onto Starkey Road.

Notifications: it’s not just texts. It’s Snapchats, Instagram alerts, and Life360 pings.

A two-second glance at a screen at 45 mph means they just drove the length of a football field blind. On our crowded roads, that’s usually where the brake lights of the car in front of them are.

The _Who Pays__ Question (And Why Parents Should Be Worried)")

Most parents assume that if their teen causes a crash, the insurance will handle it, and maybe their rates will go up. That’s the best-case scenario. But in Florida, the liability laws are very specific, and they are designed to protect the victim, not the driver or the driver's parents.

If you are a parent in Largo, you need to understand three concepts. These aren't just legal jargon; they are the things that can put your house and savings at risk.

You Signed the Contract (Statute § 322.09)

Do you remember the day you took your kid to get their learner’s permit or driver’s license? It’s a proud moment. You stood at the counter, filled out a form, and signed your name. Most people don't read the fine print on that form.

By signing that application, under Florida Statute § 322.09, you agreed to be jointly and severally liable for any negligence or willful misconduct of your minor child when they are driving.

This isn't about whether you own the car. This isn't about whether you were in the passenger seat. You essentially co-signed for their driving behavior. If they run a red light and injure someone, the law views you as equally responsible for the damages.

The "Dangerous Instrumentality" Doctrine

I know, it sounds like something out of a sci-fi movie. But Florida is one of the few states that follows this legal doctrine strictly. A car is considered a dangerous tool. Like a weapon. Because a car is dangerous, the law says the owner is responsible for how it is used. If you own the car, your name is on the title, and you give anyone permission to drive it, you are on the hook.

It doesn’t matter if you told your teen, "Drive safe."

It doesn’t matter if you said, "Don't take the interstate."

It doesn’t matter if you said, "Be home by 10."

If you gave them the keys (express permission) or even if they just took the keys and you didn't stop them (implied permission), you are liable. This catches so many parents off guard. They think, "I didn't crash the car, why am I being sued?" You are being sued because you are the owner of the dangerous instrument that caused the harm.

The "Permissive Use" Trap

This one gets complicated. Let’s say you let your son drive the car. He goes to a friend’s house. Then, he lets his friend drive your car to the store. The friend crashes. Are you liable?

In many cases, yes. Florida courts have often ruled that if you allow someone to use your car, and they allow a third person to use it, the owner is still responsible. You lose control of the liability the moment those keys leave your hand.

Why Minimum Insurance is a Disaster in Largo")